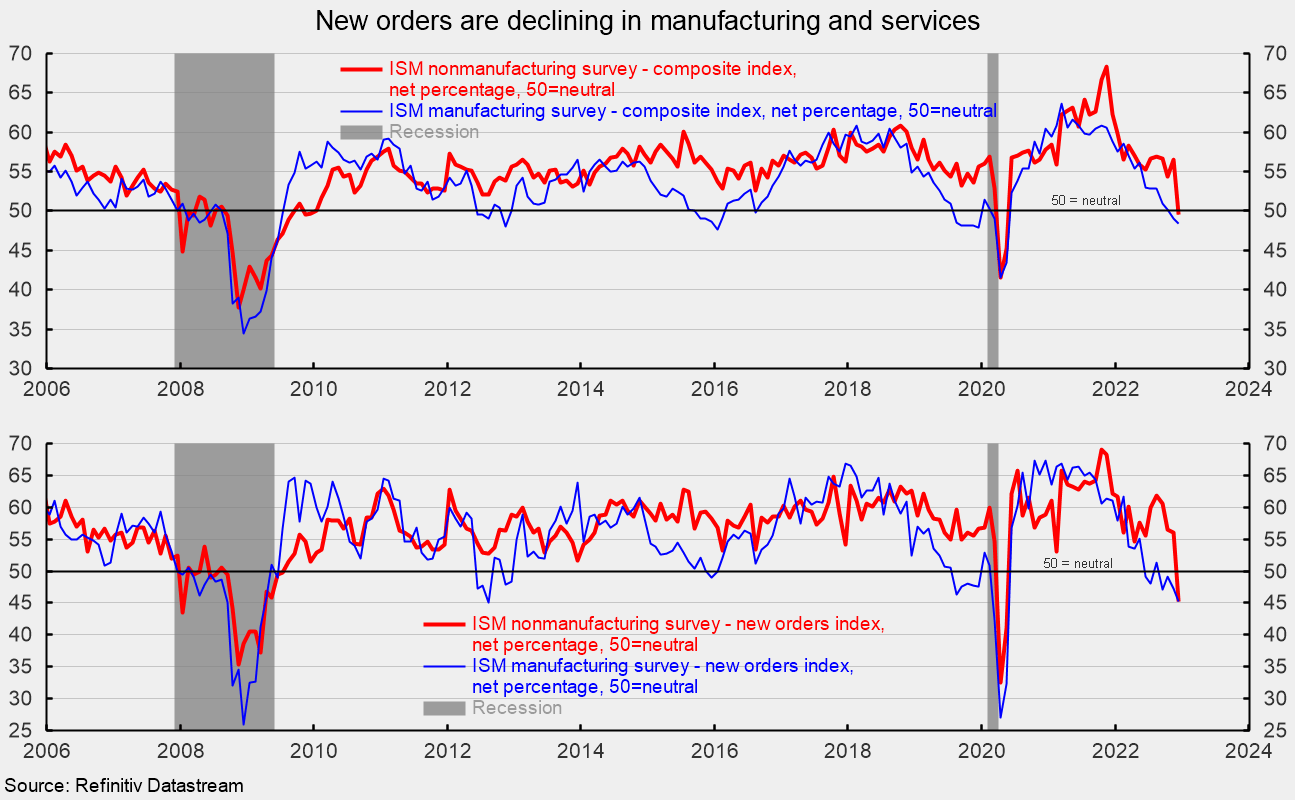

The Institute for Supply Management’s NMI composite services index decreased to 49.6 percent in December, sinking 6.9 points from 56.5 percent in the prior month. December was the first drop below the neutral 50 threshold following 30 consecutive months of expansion for the services sector (see top of first chart). The December ISM surveys suggest a contraction in the services and manufacturing sectors, a very ominous sign should the results persist in the coming months.

Among the key components of the services composite index, the business activity index plunged 10.0 points to 54.7 (see top of second chart). That is the 31st consecutive month above 50. Eleven industries reported increased activity, while four reported slower activity.

The services employment index fell in December, coming in at 49.8 percent, down from 51.5 percent in November. That is the sixth time in the last eleven months that the employment index was below neutral, with an average of 50.2 percent over that period (see bottom of second chart).

Five industries reported employment growth, while four reported a reduction. The report states, “Employment contracted due to a combination of decreased hiring due to economic uncertainty and an inability to backfill open positions.”

The services new-orders index fell to 45.2 percent from 56.0 percent in November, decreasing by 10.8 percentage points (see bottom of first and second charts). The new orders index had been above 50 percent for 30 consecutive months. The December results are now in line with weakness in new orders in the manufacturing sector (see bottom of first chart).

The nonmanufacturing new-export-orders index, a separate index that measures only orders for export, plunged in December, coming in at 47.7 versus 38.4 percent in November and the third consecutive month below neutral. Seven industries reported growth in export orders, with four reporting declines and seven reporting no change. However, of all respondents, only 27 percent said they perform and track separate activity outside the US.

Backlogs of orders in the services sector likely grew again in December though the pace is weak as the index decreased to 51.5 percent from 51.8 percent. December was the 24th month in a row with rising backlogs. Six industries reported higher backlogs in December, while four reported decreases.

Supplier deliveries, a measure of delivery times for suppliers to nonmanufacturers, came in at 48.5 percent, down from 53.8 percent in the prior month (see top of third chart). It suggests suppliers are cutting the lead time in delivering supplies to the services business. That is the lowest reading for the index since December 2015. The results for the services sector have come into alignment with the manufacturing sector results (see top of third chart). For the services sector, five industries reported slower deliveries in December, while seven reported faster deliveries.

The nonmanufacturing prices paid index fell to 67.6 percent in December from 70.0 in the prior month (see bottom of third chart). Fifteen industries reported paying higher prices for inputs in December. Price pressures have eased somewhat for the services sector, but the results over the last six months lag the easing price pressures reported by the manufacturing sector which has seen significant declines in price pressures (see bottom of third chart).

The latest Institute of Supply Management report suggests that the services sector and the broader economy contracted in December following 30 consecutive months of expansion. The results are more consistent with weakness in the manufacturing sector in recent months. Should weak results persist in both surveys, it would be an ominous sign for the overall economy. Caution is warranted.

The post Services-Sector Sees a Plunge in New Orders in December was first published by the American Institute for Economic Research (AIER), and is republished here with permission. Please support their efforts.

{kind=link}