Total nonfarm payrolls posted a 223,000 gain in December versus a 256,000 rise in November (revised down by 7,000), while October had an increase of 263,000 (revised down by 21,000). The December result beat the consensus expectation of 200,000.

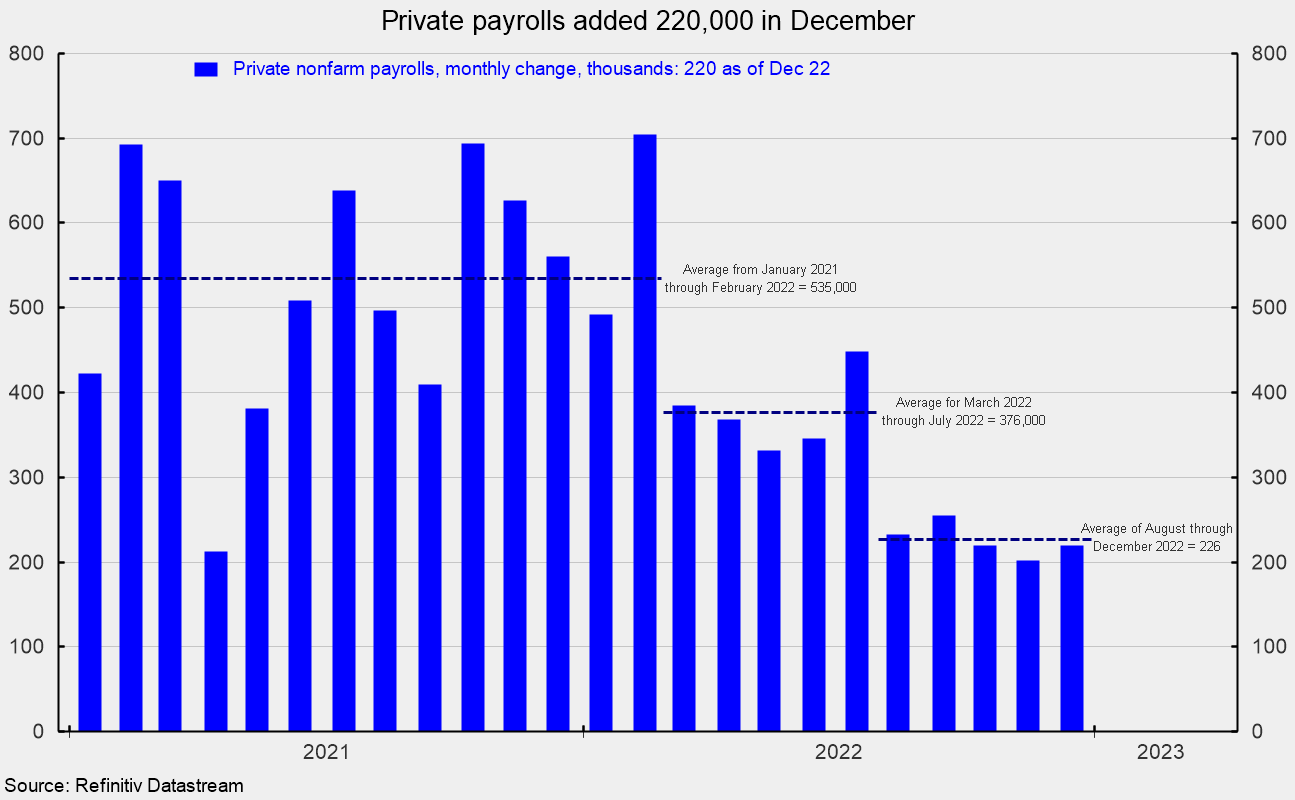

Excluding the government sector, private payrolls posted a gain of 220,000 in December after adding 202,000 jobs in November. The average monthly gain over the 24 months since January 2021 was 437,000. However, the monthly increases appear to be slowing. Over the 14 months from January 2021 through February 2022, the average monthly rise was 535,000; for the five months from March 2022 through July 2022, the average was 376,000; and over the last five months, the average has dropped to 226,000 (see first chart). The trend in payroll gains is slowing.

The results among the various industries were generally positive in December, though just two industry groups, healthcare and leisure, accounted for 64 percent of the net gain for the month. Three industries had payroll declines in December.

Within the 220,000 increase in private payrolls, private services added 180,000 versus a 12-month average of 294,900, while goods-producing industries added 40,000 versus a 12-month average of 55,300.

Within private service-producing industries, education and health services added 78,000 (versus a 79,200 twelve-month average), leisure and hospitality increased by 67,000 (versus 78,800), wholesale trade added 12,100 (versus 14,600), and retail gained 9,000 (versus 16,200; see second chart).

Within the 40,000 addition in goods-producing industries, construction added 28,000, durable-goods manufacturing rose by 24,000, and mining and logging industries added 4,000. However, nondurable-goods manufacturing reduced payrolls by 16,000, (see second chart).

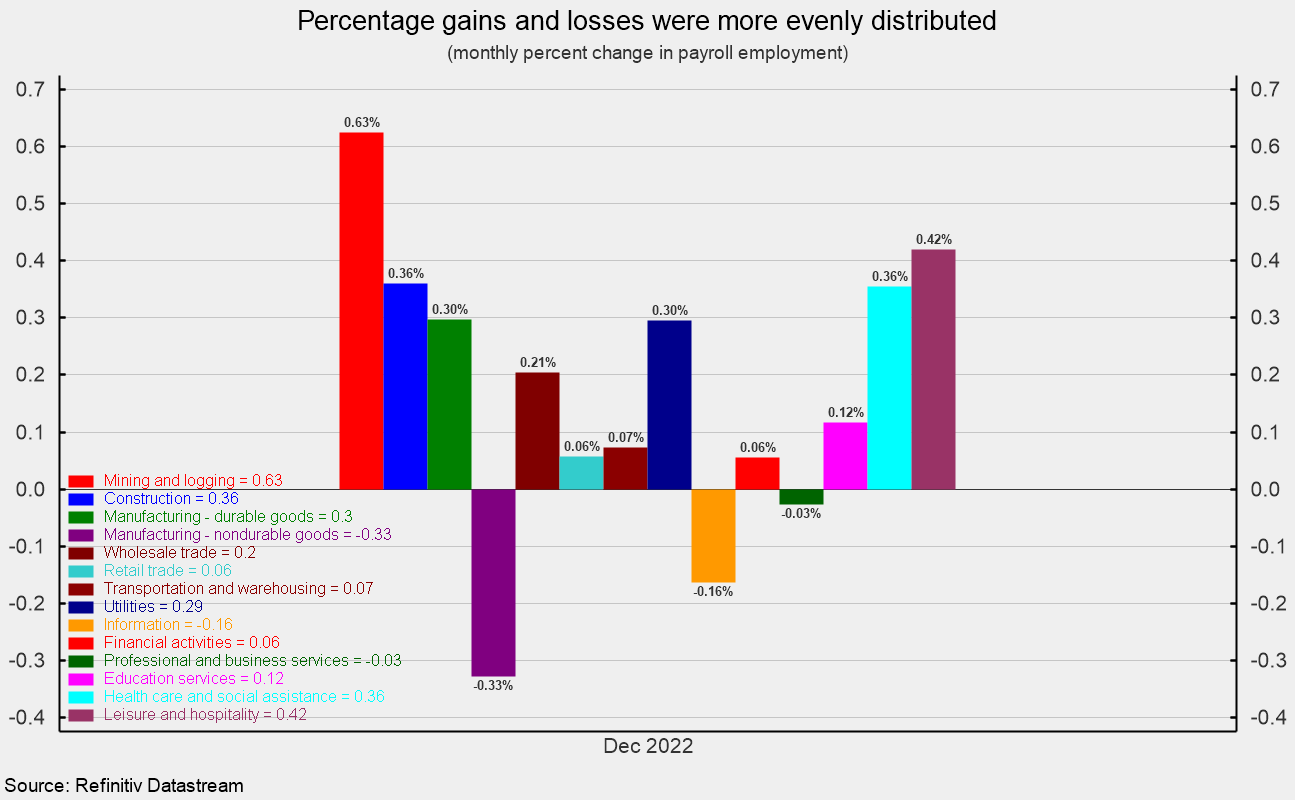

While a few of the services industries dominate actual monthly private payroll gains, monthly percent changes paint a different picture. Gains and losses were more evenly distributed, as four industries expanded payrolls by more than 0.3 percent, and three others exceeded 0.2 percent (see third chart).

Average hourly earnings for all private workers rose 0.3 percent in December (see fourth chart). That puts the 12-month gain at 4.6 percent, down from a recent peak of 5.6 percent in March 2022 and the slowest rate since August 2021 (see fourth chart). Average hourly earnings for private, production and nonsupervisory workers rose 0.2 percent for the month and are up 5.0 percent from a year ago, down from 6.7 percent in March.

The average workweek for all workers fell to 34.3 hours in December from 34.4 in November while the average workweek for production and nonsupervisory dropped to 33.8 hours versus 33.9 in the prior month.

Combining payrolls with hourly earnings and hours worked, the index of aggregate weekly payrolls for all workers gained 0.2 percent in December and is up 6.5 percent from a year ago; the index for production and nonsupervisory workers was unchanged for the month and is 7.4 percent above the year ago level.

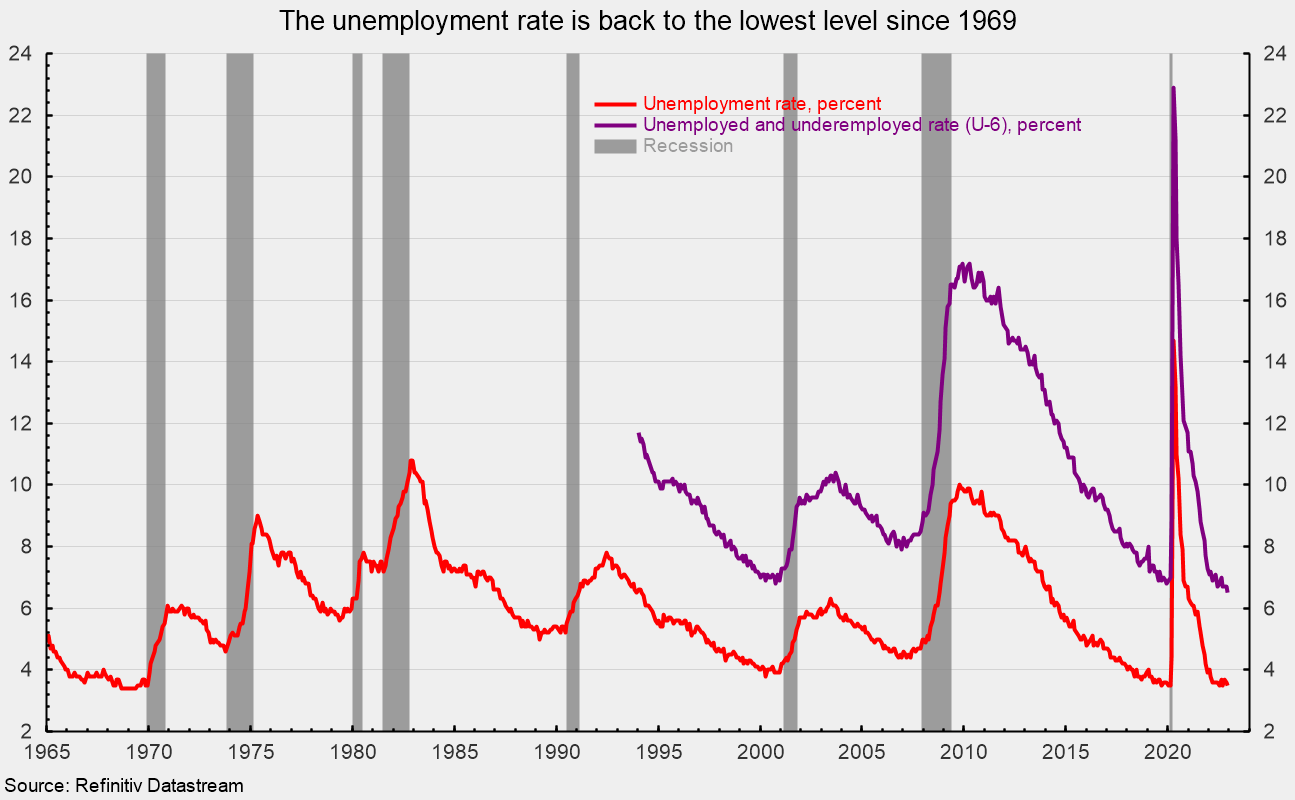

The total number of officially unemployed was 5.722 million in December, a drop of 278,000. The unemployment rate fell to 3.5 percent, matching the lowest result since 1969 (see fifth chart). The underemployed rate, referred to as the U-6 rate, decreased by 0.2 percentage points to 6.5 percent in December, a record low going back to 1995.

The employment-to-population ratio, one of AIER’s Roughly Coincident indicators, came in at 60.1 percent for December, up 0.2 from November but still significantly below the 61.2 percent in February 2020.

The labor force participation rate rose by 0.1 percentage point in December to 62.3 percent. This important measure has been trending flat recently but is still well below the 63.3 percent of February 2020 (see sixth chart).

The total labor force came in at 164.966 million, up 439,000 from the prior month and a new record high (see sixth chart). If the 63.3 percent participation rate were applied to the current working-age population of 264.844 million, an additional 2.68 million workers would be available.

The December jobs report shows total nonfarm and private payrolls posted additional gains, but the data show the trend in payroll gains is decelerating, and concerns about future payroll gains persist in light of aggressive Fed interest rate increases. Furthermore, labor force participation increased, the total labor force hit a record high, and job cut announcements are trending higher.

Conversely, the unemployment rate dropped back to a multidecade low, the level of open jobs remains high, and the number of available workers is low, suggesting the labor market remains tight despite some signs of loosening.

Persistently elevated rates of rising prices are driving aggressive Fed rate increases. At the same time, the fallout from the Russian invasion of Ukraine continues to disrupt global supply chains. Finally, the AIER Leading Indicators Index remains well below the neutral 50 threshold, suggesting an elevated level of risk for the economic outlook. Caution is warranted.

The post Labor Market Shows Early Signs of Loosening was first published by the American Institute for Economic Research (AIER), and is republished here with permission. Please support their efforts.

{kind=link}