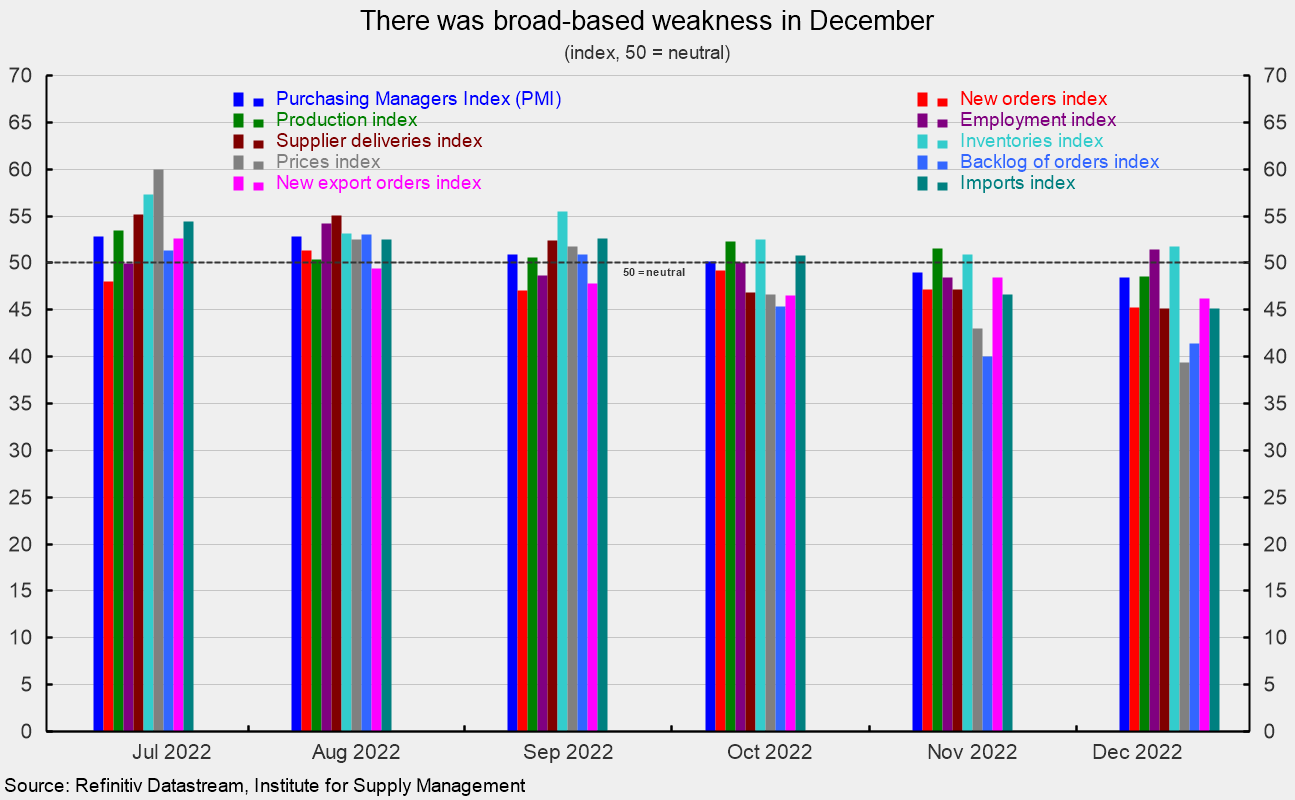

The Institute for Supply Management’s Manufacturing Purchasing Managers’ Index fell to 48.4 percent in December, the second consecutive reading below neutral and the lowest level since May 2020. The survey suggests the manufacturing sector contracted in December (see the first chart).

Nearly every component index was below neutral for the month (see second chart). According to the report, “The U.S. manufacturing sector again contracted, with the Manufacturing PMI at its lowest level since the coronavirus pandemic recovery began. With Business Survey Committee panelists reporting softening new order rates over the previous seven months, the December composite index reading reflects companies’ slowing their output.”

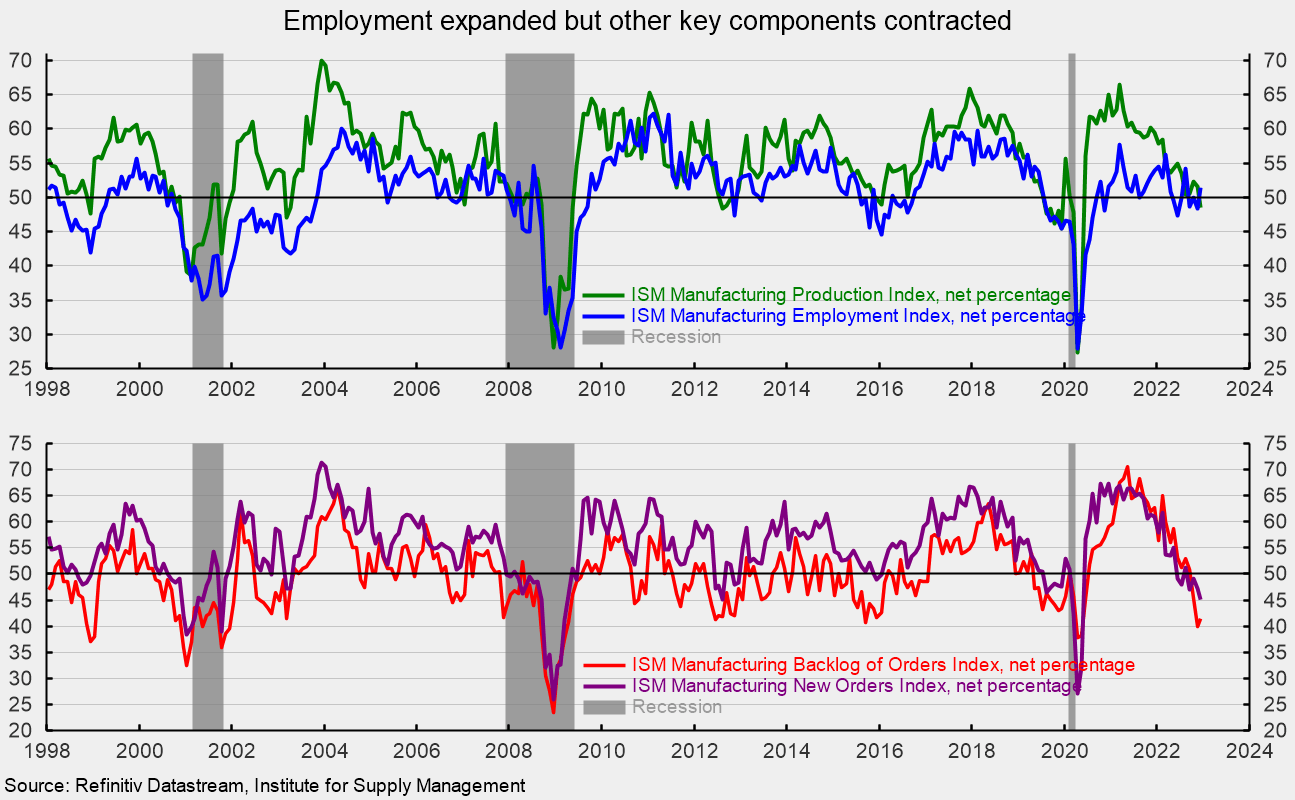

The Production Index fell below neutral, suggesting contraction for the month. The index came in at 48.5 percent in December, falling 3.0 points from November (see the top of the third chart). The index had been above 50 for 30 months and is well below its 25-year average of 55.4 percent.

The Employment Index rose to 51.4 percent, adding 3.0 points. The December result was the third time in the last eight months that the index was above neutral, averaging 49.9 over that span (see the top of the third chart). The report states, “Many panelists’ companies confirm that they are continuing to manage head counts through a combination of hiring freezes, employee attrition and layoffs.”

The Bureau of Labor Statistics’ Employment Situation report for December is due out Friday, January 6, and expectations are for a gain of 200,000 nonfarm payroll jobs, including the addition of 10,000 jobs in manufacturing.

The new orders index fell by 2.0 points posting its fourth consecutive month and the sixth month in the last seven below the neutral 50 mark. The index came in at 45.2 percent (see the bottom of the third chart). According to the report, “Of the six largest manufacturing sectors, only Transportation Equipment reported increased new orders.”

The new export orders index, a separate measure from new orders, fell in December, dropping to 46.2 percent versus 48.4 percent in November. The latest reading is the fifth consecutive month below 50.

The Backlog-of-Orders Index came in at 41.4 percent versus 40.0 percent in November, a 1.4-point rise (see the bottom of the third chart). This measure has pulled back from the record-high 70.6 percent result in May 2021 and is below neutral for a third consecutive month, suggesting a contraction in backlogs. Two of eighteen industries reported a decline in backlogs, while twelve reported growth.

Customer inventories in December are considered “about right”, with the index dropping to 48.2 percent, very close to the neutral 50 level (index results below 50 indicate customers’ inventories are too low). According to the report, “The current index level continues to no longer provide positive support to future manufacturing expansion.”

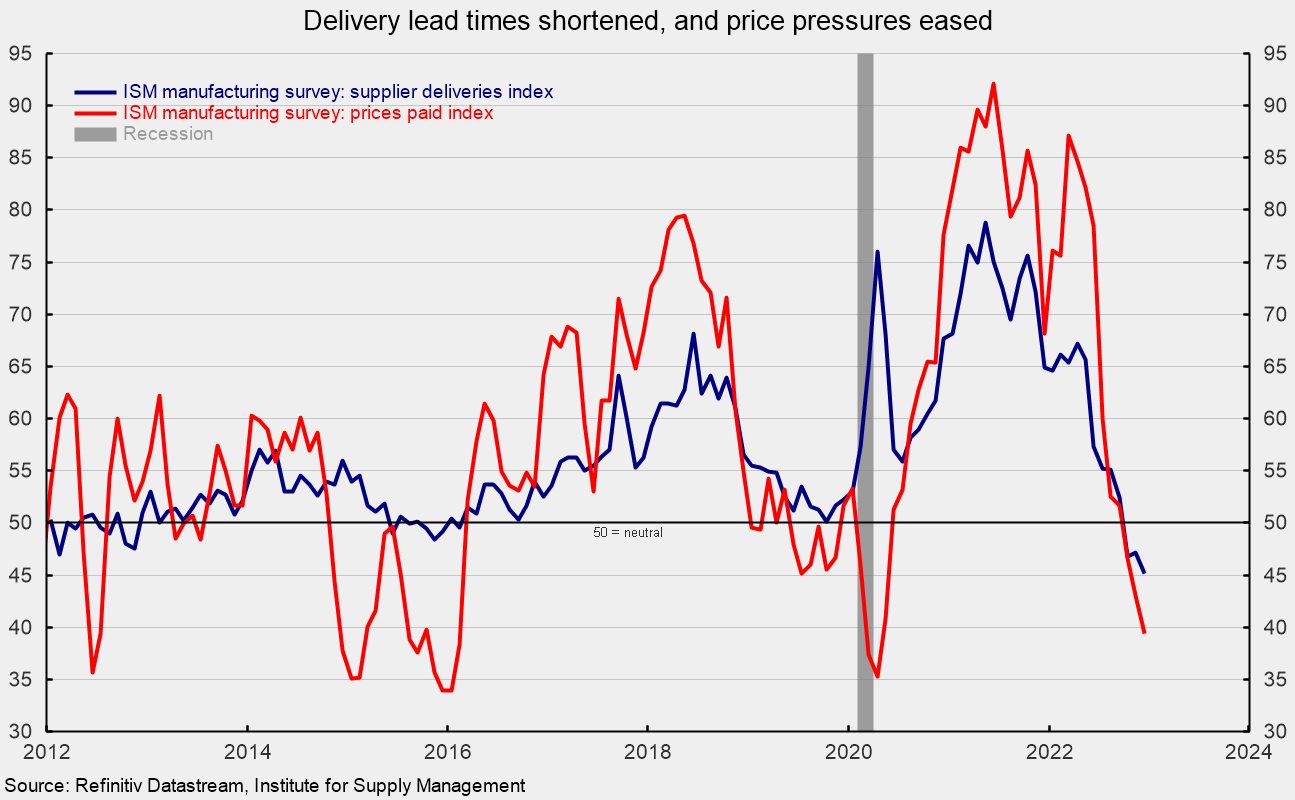

The supplier deliveries index registered a 45.1 percent result in December, off 2.1 points from November. December was the third month below 50 and suggests shortening lead times for delivery of input materials (see fourth chart).

The index for prices for input materials sank again, dropping another 3.6 points to 39.4 in December (see fourth chart). The index is down from 87.1 percent in March 2022 and 92.1 percent in June 2021. The result suggests input prices may have declined for the third consecutive month in December.

The survey suggests the manufacturing sector has seen a clear slowdown in recent months with broad based weakness across different aspects of business. Economic risks remain elevated due to the impact of inflation, an aggressive Fed tightening cycle, continued fallout from the Russian invasion of Ukraine, and waves of new Covid-19 cases in China. The outlook remains highly uncertain. Caution is warranted.

The post Manufacturing-Sector Contracts Again in December was first published by the American Institute for Economic Research (AIER), and is republished here with permission. Please support their efforts.

{kind=link}